2025 Gasoline & Ethers Outlook - A non-commercial review of potential changes to supply & demand fundamentals and product trade flows

In our first newsletter for the year we would like to share our views and thoughts on latest trends, developments and changes in global gasoline and ethers markets and their impact on regional supply & demand balances and product trade flows. This non-commercial review focuses on the main regulatory aspects and adjustments to production capacity in 2024/2025.

Introduction - Geopolitical events in 2024/2025

Over the last few years global energy markets have been affected by the ongoing war between Russia and the Ukraine, the raging Middle East crisis and escalating trade conflicts between the world’s super powers. 2024 was no exception, whereas 2025 promises to bring some changes. The recent ceasefire between Israel and Hezbollah de-escalated the situation in Middle East, and the US push for an end of the Russia-Ukraine war may also help to stabilize world peace.

Global economies have been fighting inflation over the last two years, and interest rates are finally starting to come down. Consumer confidence and spending is gradually improving, also in China, which however still has a long way to go for a full recovery. In January 2025 Donald Trump took office as the 47th US President for a 2nd time and his reinstatement rattled global markets with spontaneous tariff and embargo announcements and their withdrawals, adding a new level of uncertainty to the global energy markets. Sanctions and embargoes on vessels and entire fleets have already caused significant increases in freight cost, which were already inflated by the crisis in the Middle East.

The next COP meeting will be held in November 2025 in Brazil and many countries are still far away from their intended climate improvement targets. Air pollution remains a global challenge with large parts of the world remaining exposed to heightened health risks.

China – Gasoline consumption is set to decline, weighing on clean fuels demand

China's economy has been struggling to recover since the COVID pandemic, largely due to the ongoing crisis in the real estate industry, which was felt across many other industries. After multiple fiscal stimulus measures have been implemented by Beijing over the last couple of years, we can now see some signs of growing consumer confidence and a recovery in the propensity to consume.

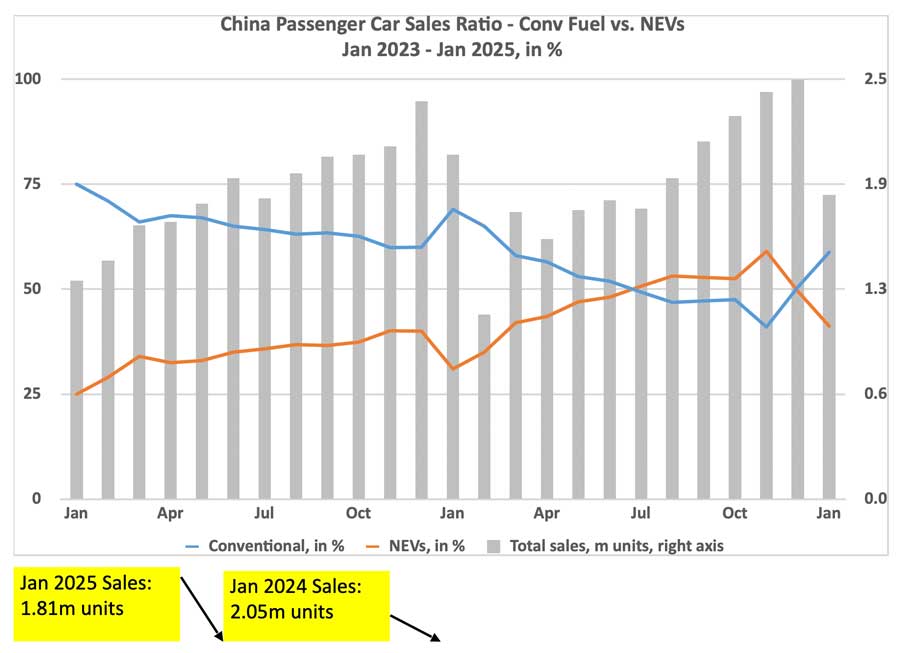

However, market insiders and industry analysts point out that gasoline demand in the country has peaked in 2024 and is now expected to gradually decline forward. This is predominantly caused by the government’s increased push for electrification of the country’s transportation fuel sector. In terms of registration of new passenger cars, the market share for electric vehicles, including hybrid fuel-cell cars, has surpassed conventional fuel-type cars for the first time in 2024 and is expected to grow further from here on forward, as Beijing continues to make fiscal stimulus measures for the new-energy industry and its consumers available. Industry reports forecast that the registration share for new energy vehicles (NEVs) will grow to 57% of all new passenger cars in 2025. The oil industry estimates that NEVs have undercut around 250,000-300,000 bpd of oil demand growth in 2024, while use of compressed and LNG in road freight displaced around 150,000 bpd.

The chart underneath shows the January 2023 - January 2025 sales data for new passenger cars and their market share split between NEVs and conventional other fuel car types in China.

(Source: Data from China Passenger Car Association, February 2025)

Gasoline quality requirements in China remain among the world’s leading standards. Current GB-6a and GB-6b specifications, which are equivalent to Euro-6, are intended to be upgraded to GB-7 in 2030, which will bring further restrictions for environmentally harmful components and additives.

MTBE has benefited significantly from the improvement in gasoline quality in China over the past 15 years, but lower gasoline consumption in the future will also reduce demand for clean fuels, including MTBE. At present MTBE is blended into China’s domestic gasoline supply at a rate of around 9%, being also one of the highest worldwide.

Apart from the decline in domestic gasoline consumption, fuel and MTBE production capacity in China increased further in 2024 and it is widely expected that China will push incremental quantities into the export markets, which are already struggling with increased supplies from China. MTBE deliveries have become a regular feature in Europe, and gasoline shipments reach as far away as Africa and Mexico.

Nigeria – Dangote refinery started up in 2024

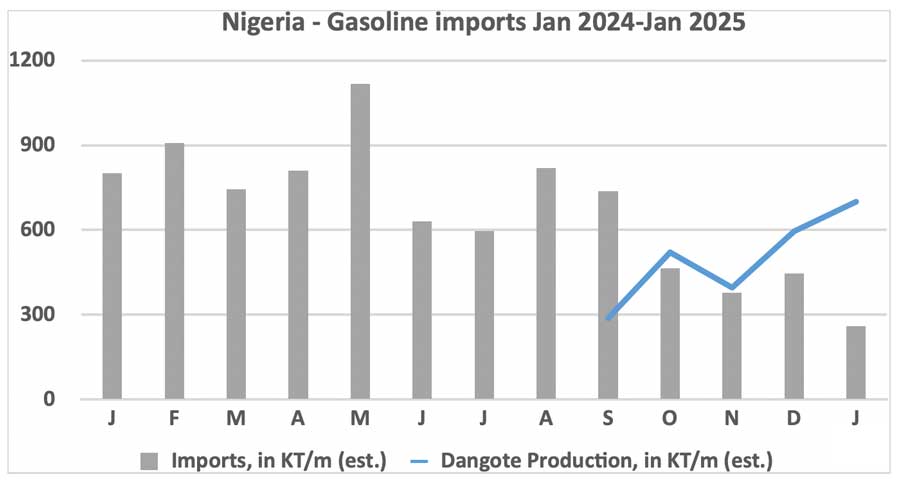

After years of delay Nigeria’s Dangote refinery, which has a nameplate capacity of 650,000 bpd and is one of the world’s top-10 refineries, was commissioned in January 2024, and the unit’s gasoline production started up in September 2024. Currently running at around 85%, the refinery recently announced to reach full gasoline production capacity in due course.

After a number of hiccups during the start-up phase and as crude input was also inconsistent, Dangote currently supplies about 700,000 MT a month or nearly 60% of the country’s total gasoline demand (estimated at 1.25m MT/month on average) and has already begun to export small quantities of around 100KT a month to neighbouring markets in West Africa.

Once operating reliably, Nigeria will disappear as a large-scale gasoline importer, which has already started to impact the European fuel export market in particular. Over the last few years Europe has supplied more than 10m MT of gasoline to Nigeria each year, and this is changing drastically. Dangote will be able to comply with recent quality improvements (reduced Sulphur, lower Benzene) and other regulations (non-oxy standards) in Nigeria, reducing import quantity and quality requirements.

Estimated import demand in 2025 is down to around 3.0m MT and appears to be set to decline further beyond. While operating rates remain dependent on the complexity of the refinery and as crude oil availability may fluctuate, import demand may occur sporadically. However, the regular product import supply flow will be curtailed significantly.

The chart underneath shows how the Dangote start-up has impacted gasoline imports between January 2024 and January 2025.

(Source: DK&A Clean Fuels Barometer newsletter, February 2025)

The reduced gasoline import demand and specification changes for imported gasoline will also weigh on Europe’s conventional MTBE demand, as less supply of the clean fuel will be required. While MTBE is not needed in Nigerian gasoline supplies, the clean fuel has been used regularly in the past as a mean to comply with specification requirements.

Europe – challenges for gasoline blending, opportunities for sustainable fuels

Responding to the sharp decline in demand from Nigeria and elsewhere in West Africa, a number of European refineries are closing down or are considering this step, also as their competitiveness is increasingly challenged. Gasoline blenders in ARA have already prepared for the demand drop, after interest in this business segment dropped over the last two years, when margins were increasingly squeezed and as blending became a more complicated task.

In 2024 the Netherlands and Belgium implemented new regulations on specification limits and the use of a number of components in gasoline export blending. The export of low-quality gasoline to West Africa has been affected by the reduction of the maximum Sulphur content from 1500 ppm to just 50 ppm, whereas the allowed Manganese content has been reduced to 2mg/litre only. In particular, the cap on allowed Benzene of 1% only made blending operations less attractive, reducing the max volume of pyrolysis gasoline (Pygas) in the blend, which is typically priced at a decent discount to gasoline itself. This already had a notable impact on the quantity of MTBE used, as the octane-loss of Pygas weighed less than before, when the product was replaced by higher-octane rating products.

Shipments to West Africa are now increasingly covered by European refinery supplies directly, as blenders focus more on markets across the Atlantic or to other parts of the world.

Overall, the drop in demand from West Africa will elevate the gasoline supply surplus in Europe, as access to i.e. North Africa and the Middle East has also been challenged by incremental deliveries ex Russia and, of course, by increased refining capacity in both regions. The recently announced six-month ban on gasoline exports from Russia was received as welcome news, but Russian gasoline producers themselves are allowed to continue exporting.

While demand for conventional MTBE in Europe will be challenged by the afore-mentioned changes to export flows for gasoline, the situation for renewable MTBE (bio-MTBE) and bio-ETBE in Europe may provide some support, as current ether production may have to make up for potential demand increases. Both products qualify for fuel blending in Europe’s domestic gasoline pool, complying with sustainability standards and greenhouse gas (GHG) intensity limits, recently introduced as part of the EURO-7 emission standard roll-out.

India – Implementing E20 standards ahead of schedule

India is striving to roll out the government’s E20 gasoline-blending mandate by March, nine months ahead of schedule, given enough availability of the biofuel in the domestic market without endangering sugar production, and state-owned oil marketing companies, which represent more than 90% of the market, are targeting to achieve a 20% Ethanol blending rate in their domestic gasoline supply next month.

India’s Petroleum and Natural Gas Minister Hardeep Singh Puri said at the Auto Expo 2025 on 21- January this year that India will achieve 20% blending of Ethanol in gasoline in the next two months and will soon be able to blend more than 20% Ethanol into gasoline if the need arises.

India’s petroleum product consumption, led by solid increases in gasoline demand, has been growing solidly in 2024, but market analysts and consultants highlight that the steep growth in the Ethanol blending percentage will account for around 90% of the country’s total gasoline demand increase this year, leaving only a marginal incline for the fossil fuel itself. As a result of this, India’s gasoline exports are expected to remain steady this year.

While a higher Ethanol blending mandate may appear as disadvantageous for the use of ethers in gasoline, products such as bio-MTBE and bio-ETBE may still have a future in the country, as India shows no sign of stopping its strive towards a higher biofuel proportion in the gasoline mix.

Oil companies are actively looking at utilizing MTBE and bio-ETBE in their fuel pool, after a government consultancy study in 2023/2024 showed the benefits of those two clean fuels for India’s gasoline.

Current gasoline specification and emission standards in India are Bharat-6, another equivalent to Euro-6, which were rolled out nationwide in 2020. However, higher octane requirements will be needed to improve the success changes for fuel-ethers.

Mexico – Dos Bocas refinery continues to severely underperform

Gasoline and MTBE trade flows from the US into Mexico were set for a drastic decline when Pemex’s Dos Bocas refinery finally started up production during the 2nd half of 2024. However, the 340,000 bpd refinery complex continued to experience production outages ever since, caused by integration problems of various subsections and electric and design faults, among others. The unit has a gasoline production capacity of 170,000 bpd but has only managed to produce output at a fraction of this level.

Latest reports show that Pemex’s Olmeca refinery cost the country more than $20bn, compared to its original budget of just $8bn. The current production problems appear to persist and the country is still a long way from achieving its goal of “energy sovereignty”. Additional challenges are now mounting, after Donald Trump threatened to impose a 25% import tariff on crude supplies from Mexico, which were however temporarily revoked.

Gasoline imports have gradually but only marginally declined in recent years, as the country’s overall product output increased slightly but Mexico remains miles away from self-sufficiency. In November 2024 Mexico’s five refineries only produced 235,000 bpd of gasoline, its lowest for the year. Olmeca’s contribution is believed to be a mere 1.200 bpd. During the month Pemex imported around 360,000 bpd of gasoline. Olmeca’s throughput averaged <20% in November, mainly producing coke and Diesel.

The Dos Bocas refinery has a small MTBE unit in its design, but a possible start-up of the etherification plant is currently not even being considered.

US gasoline supplies, which were expected to taper off sharply, have remained at elevated levels since the Olmeca start-up, and MTBE in the USGC benefits from Mexico’s high-blending percentage of the oxyfuel. For 2025 and relying on widespread opinion that Olmeca will not achieve regular operations, blended gasoline and neat MTBE demand from Mexico is expected to stay high, which is a relief for both products, facing challenges in other regions. Beyond this, Mexico may seek incremental import supplies from Europe as well as China and elsewhere in Asia.

However, for US MTBE producers the outlook remains uncertain, as the eventual production increase in Mexico will reduce clean, high-octane demand. Today it appears difficult to replace the potential demand drop elsewhere, as ether markets in Europe and Asia appear to be fully saturated with supply and overall demand is unlikely to substantially grow. Some US producers may need to reconsider their situation long-term, in case production margin will decrease.

Conclusion

2025 will remain a challenging year for gasoline and fuel ethers as demand begins to decline in some key regions, while other main markets are expected to be stagnant at best. However, gasoline demand in parts of South-East Asia, the Middle East and Africa may continue to grow and ongoing efforts to improve fuel quality standards can provide support for clean fuels, such as MTBE and bio-ETBE.

The overall fuel demand decline, led by China, needs to be taken as a fact, but increased quality requirements will provide opportunities for sustainable fuels to be taken as part of the overall solution to improve emissions and air quality today and also beyond 2030.

In this issue of our “In Conversation with” we talked to Mr. Jeff Hove, acting Vice President and Executive Director at the Fuels Institute. In recent years we have seen some initiatives to consider policies to ban the sale of vehicles equipped with internal combustion engines (ICE), predominantly emerging in Europe, but also spreading out in parts of Asia.

In this issue of our “In Conversation with” we talked to Dr Tilak Doshi, an energy sector consultant based in Singapore. Dr Doshi shared his views and observations about the global “2050 decarbonisation” plan and move towards Electric Vehicles (EVs) with us. We would like to thank Dr Doshi for his efforts to comprehensively answer our questions which provide some highly valuable and very interesting insights into this matter, highlighting a range of topics often overlooked in the political discussion between the various stakeholders in the race to save the world from impending climate catastrophe.

In this issue of our “In Conversation with” we talked to Dr Sanjay C Kuttan, Chairman of the Sustainable Infrastructure Committee at Sustainable Energy Association of Singapore (SEAS).

.svg)

.svg)