US gasoline market – change in consumer behaviour comes at a price

Introduction:

On 01-January 2017 the new low-Sulphur Tier III gasoline standard was implemented in the US. Sulphur contents under the new specification was reduced from max 30ppm to max 10ppm. People with knowledge of the matter warned about a possible premium price increase due to the apparent octane loss caused by the specification change. While experts’ opinion about the actual octane loss remains in a rather wide range (0.5 to 3.0 octane points), it is something that refiners and blenders have to deal with. Most refiners will achieve these levels by treating the dominant source of Sulphur in the gasoline pool which is catalytic gasoline from the FCC unit. While not a major obstacle for most refiners, catalytic gasoline-treating effectively reduces Sulphur levels but also lowers the octane of the product by converting olefin into paraffin molecules.

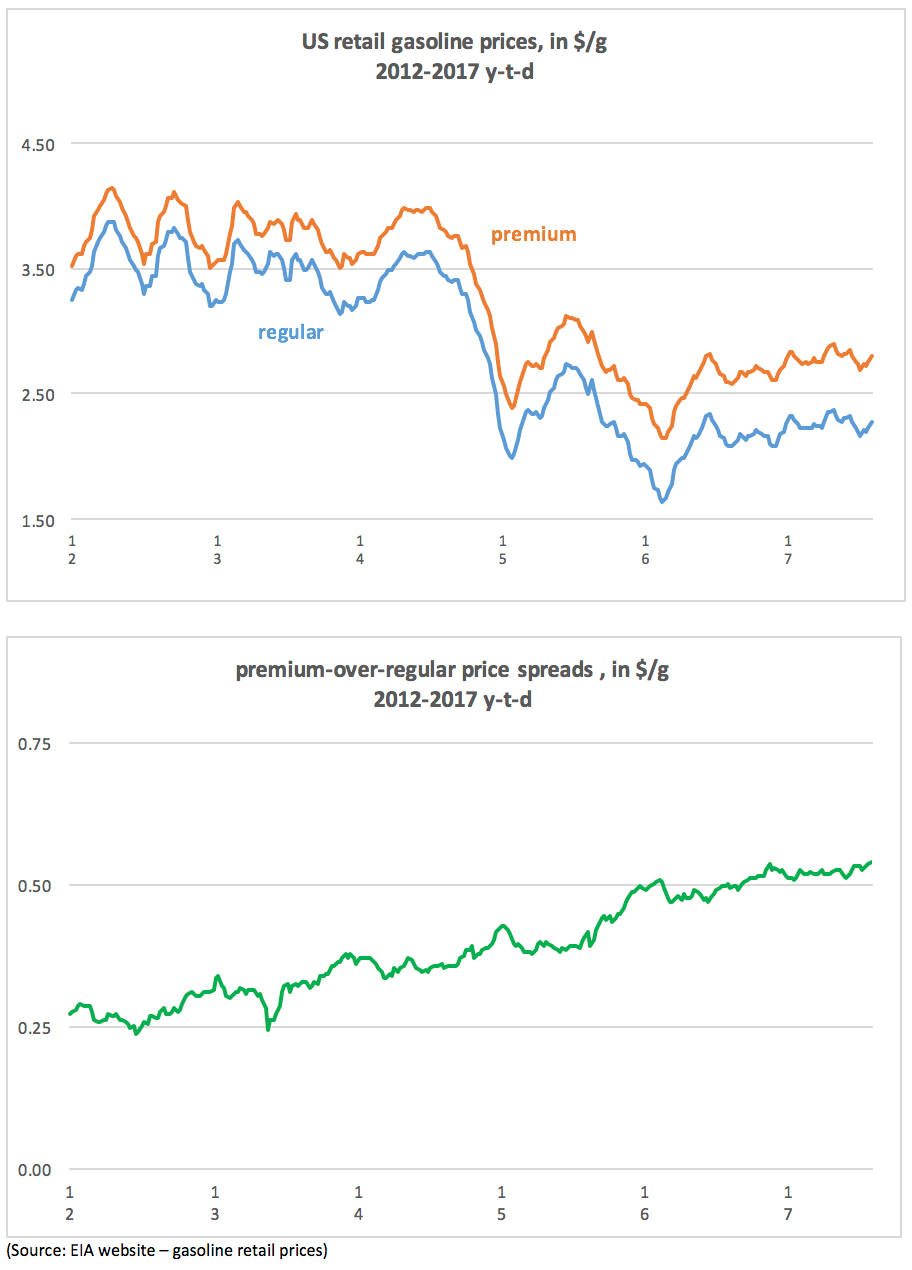

As a result we have seen consumer prices for 93(*)-premium conventional gasoline widening the gap over 87(*)-regular conventional gasoline, a trend which has already started to develop in 2012 anyway when consumer behaviour changed and motorists shifted gradually from regular to premium gasoline. The two charts underneath illustrate the retail price development for regular and premium gasoline and the spread trend between the two grades, from 2012 till date.

(*) = in the US the octane rating is indicated by AKI = (RON+MON)/2

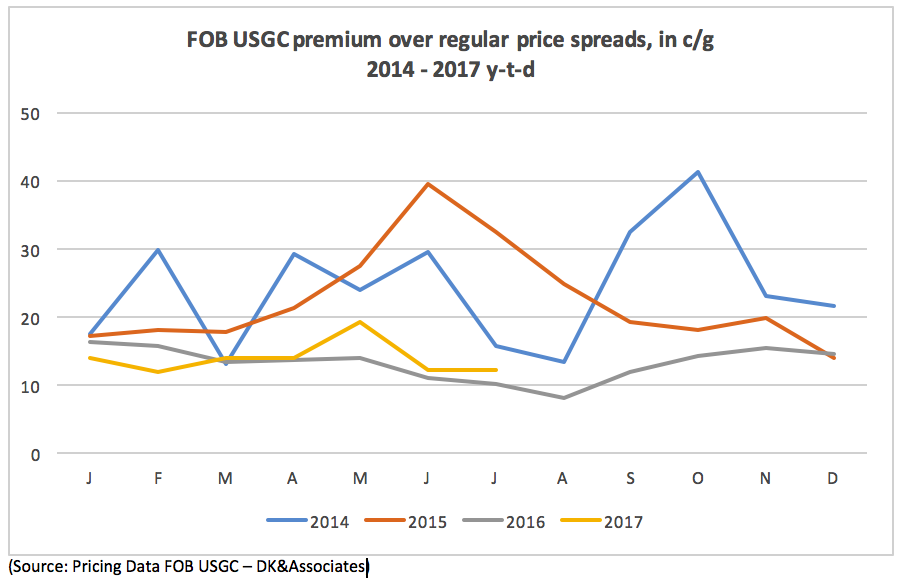

On the other hand, when looking at the price spread development in the wholesale market, the message appears rather contradictory. Price differentials between premium conventional and regular conventional have actually come down over the last 24 months, suggesting that the cost for octane has not increased at refiner/blender level. Indeed, when benchmarking gasoline blending components which are used as octane boosters against the underlying gasoline price, the same story emerges, showing no cost increase for the refiner/blender. The cost of producing higher octane grades does not produce high premiums automatically but rather supports acceptable premium pricing in the retail market. However, it must be noted that the wholesale market development is subject to other factors and cannot be directly translated into a cents per gallon price change for the consumer. The chart underneath shows the premium-over-regular spread in the US Gulf coast wholesale market from 2014 till date.

Change in consumer behaviour

Since late 2016 the price difference between U.S. average retail prices for premium and regular gasoline reached 50 cents per gallon in late 2016, and has remained above this level ever since. This price difference, or spread, has been generally increasing since 2000. Many factors on both the supply and demand sides are influencing this trend.

One of the main performance characteristics of motor gasoline is octane, a measure of gasoline’s resistance to spontaneous combustion. In the United States, retail gasoline is usually classified by its octane rating: regular gasoline with a typical octane rating of 87 is the least expensive option, and premium gasoline with a typical octane rating of 93 is the most expensive option. The price spread between the two grades of gasoline is most often representative of the cost to produce the additional octane.

On the demand side, the premium gasoline share of total motor gasoline sales has steadily increased in recent years, reaching a high of nearly 12% in August 2016—the highest share since 2004.

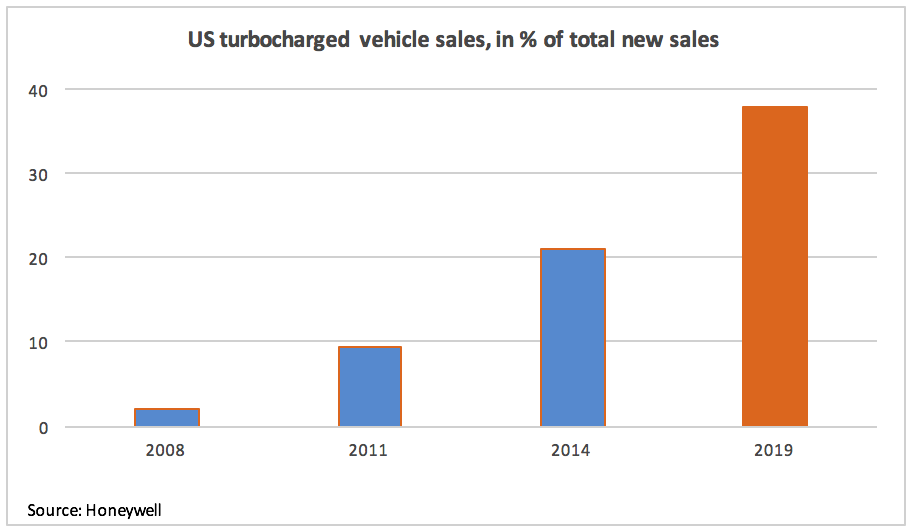

Although overall lower gasoline prices may be making premium gasoline more affordable and attractive, thereby encouraging demand, the upward trend in premium gasoline sales is more likely driven by changes in fuel requirements for light-duty vehicles in response to increasing fuel economy standards. To meet these standards, more car manufacturers are producing models with turbocharged engines that may require or recommend the use of high-octane gasoline. The following chart shows how turbo-charged vehicle sales have developed in the United States.

The primary global provider for turbocharging technology is Honeywell Transportation Systems. Honeywell is forecasting continued growth for turbocharged engines, not just in the U.S., but also in numerous other countries, such as China. Within North America, Honeywell indicates that turbocharged vehicle sales have grown from only 2% in 2008 to 21% in 2014 (this includes turbocharged diesel engines). Honeywell expects this to jump to 38% in 2019. As a result of this initiative, it seems likely that premium gasoline sales will continue to rise through the near future due to technological requirements for fuel economy and consumer preferences.

Supporting the steeply growing market share for turbocharged vehicles is the Corporate Average Fuel Economy (CAFE) program. CAFE is requiring increasingly higher mileage standards for new vehicles, forcing automobile companies to adopt a series of technologies to achieve compliance. Turbocharging has the ability to not only improve fuel economy but also engine performance.

In 2009, Ford introduced its 3.5l-V6 EcoBoost engine as an option for a number of its auto lines. While turbocharged engines had been available for decades, the higher costs of the engines generally restricted their use to sports cars and higher-end foreign models. With additional engines introduced in 2010 and 2011, Ford began utilizing this technology in increasing numbers of its U.S. sales. By 2013, nearly 80% of Ford’s vehicle lines had the option for EcoBoost engines.

International octane standards

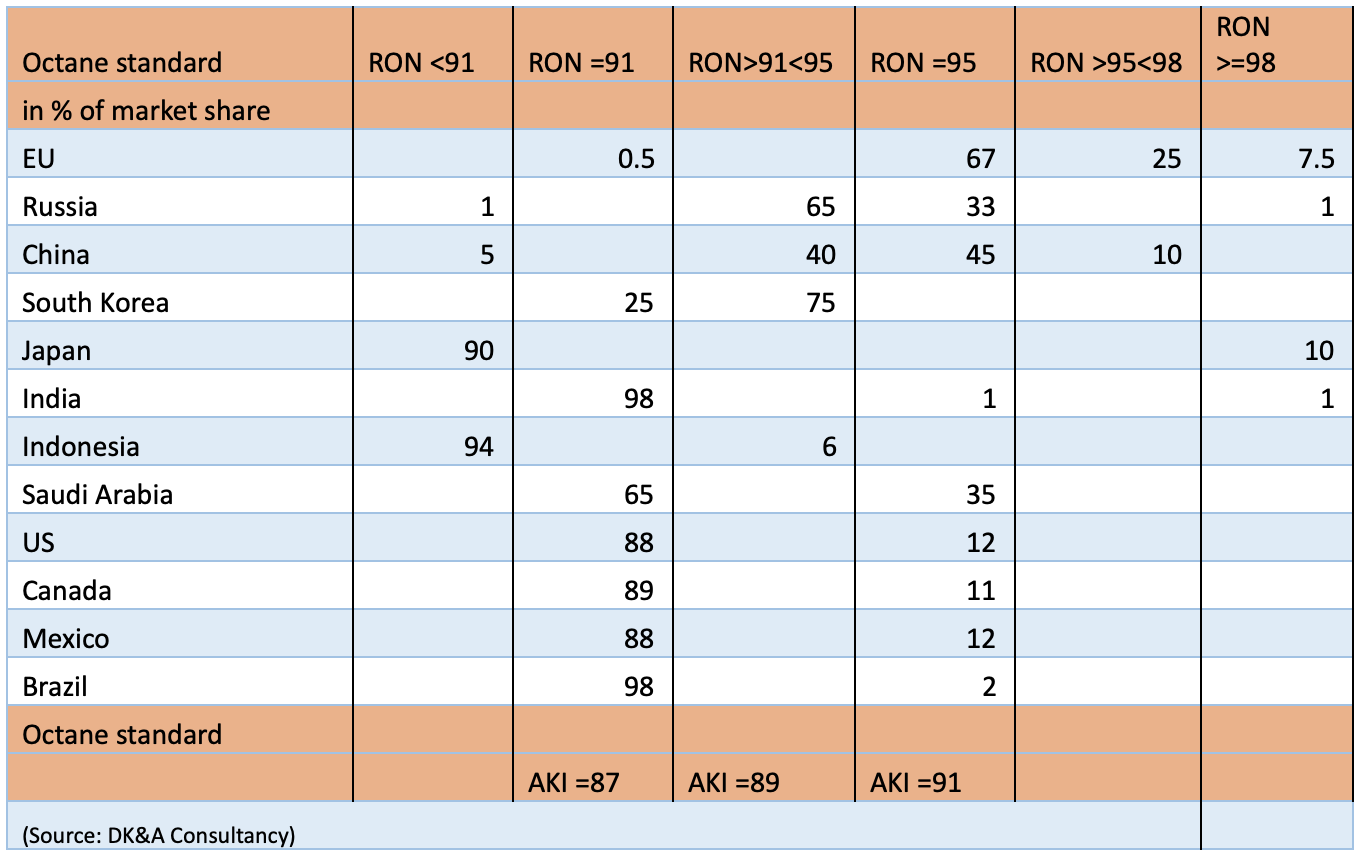

When comparing US octane standards to the rest of the world it becomes apparent that US standards are nowhere near what can be found in other regions, bearing in mind that the US refiners have less options in terms of other high quality, clean octane like ethers (MTBE, ETBE) which may hence be the cause for higher premiums.

The chart underneath illustrates the use of different octane grades in global markets, showing that standards and requirements are significantly higher in i.e. the European Union and parts of Asia. Further octane advances are expected to come from the Middle East and other parts of Asia which are on track to adopt the European 95RON standards.

Different approaches to indicate and measure the octane rating of gasoline are being applied, with the US and Latin America expressing the octane rating by AKI (antiknock index) which is calculated as (RON+MON)/2, while the rest of the world focuses on the research octane number (RON) alone. For our readers’ understanding and use of the table underneath, a gasoline quality of AKI 91 corresponds to RON 95 gasoline (Premium Unleaded in Europe), while AKI 87 is equivalent to RON 91 quality (Regular Unleaded in Europe).

The %-market share has been clustered into the most widely used octane ranges/market segments in the international markets.

The role of fuel-Ethanol in the United States

This long-running trend of higher demand for premium gasoline in the United States has occurred at the same time as costs to produce and supply octane for gasoline have increased. American energy policy reforms in recent years have promoted the widespread use of fuel-Ethanol as a source of octane in gasoline. However, there is limited demand for, and challenges associated with, blending Ethanol into gasoline in concentrations >10%. Ethanol inputs as a percentage of total gasoline consumed approached the 10% blend wall already in 2013 and have since plateaued, even as the demand for higher octane blends increased.

It had been proposed by experts that the combination of increasing demand for premium gasoline and market challenges to further increase Ethanol blending has led refiners and blenders to acquire more expensive sources of octane. The fact that US refiners have no other options like ethers had led to an increase in the price differential between premium and regular gasoline in recent years.

Even if the EPA forces greater volumes of Ethanol into the gasoline pool, a potential octane shortage may not be averted. If E85 becomes the preferred path, the additional octane from the Ethanol will not be fully utilized as typical E85 has an AKI octane number, much higher than premium gasoline and hence results in an inefficient use of the incremental octane supply.

Conclusion

Beyond Ethanol, other sources of high-octane blending components are produced by downstream units at petroleum refineries. Although total distillation capacity has increased in recent years, there has not been a corresponding increase in high-octane refining units. Compared to other global markets and due to the unique refinery configuration, US refiners have less available options to produce high-octane blending components.

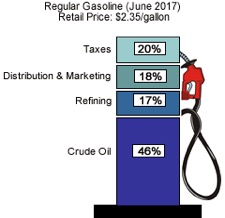

In the United States, the cost per gallon of gasoline for the consumer is a very different composition than we have i.e. in Europe where the tax burden takes the by far biggest slice of the cake. In the US, the impact of octane and quality improvements will be much more directly noticed and the share of refining cost in the graphic below will potentially grow in the future.

(Source: EIA website, US Energy Information Administration)

Change in consumer behaviour

The consumer trend towards higher gasoline octane grades is likely to continue in the US in the future and high quality, clean octane will become more important and more highly valued. Based on the above arguments it will need to be seen whether this will ultimately lead to a further price drift between regular and premium gasoline. Naturally any quality improvement will come at a price but the octane supply and supply cost do not underpin this argument.

Upgrading octane grades is a trend that allows the introduction of smaller, more powerful engines to meet new fuel economy targets.

The shift to higher octane fuels is not just occurring in North America, but in many other regions as well. Driven by the same desire to improve fuel economies and qualities, large parts of Asia are adopting the European standard of 95RON gasoline. Today, US gasoline standards in terms of octane as well as market share distribution are trailing well behind the reference fuels of Euro V/VI and this gap may grow further with the positive initiatives undertaken in Asia.

In this issue of our “In Conversation with” we talked to Mr. Jeff Hove, acting Vice President and Executive Director at the Fuels Institute. In recent years we have seen some initiatives to consider policies to ban the sale of vehicles equipped with internal combustion engines (ICE), predominantly emerging in Europe, but also spreading out in parts of Asia.

In this issue of our “In Conversation with” we talked to Dr Tilak Doshi, an energy sector consultant based in Singapore. Dr Doshi shared his views and observations about the global “2050 decarbonisation” plan and move towards Electric Vehicles (EVs) with us. We would like to thank Dr Doshi for his efforts to comprehensively answer our questions which provide some highly valuable and very interesting insights into this matter, highlighting a range of topics often overlooked in the political discussion between the various stakeholders in the race to save the world from impending climate catastrophe.

In this issue of our “In Conversation with” we talked to Dr Sanjay C Kuttan, Chairman of the Sustainable Infrastructure Committee at Sustainable Energy Association of Singapore (SEAS).

.svg)

.svg)